So far, so good, but what now for 2021?

It has been a good first half of the year for investors, driven by reopening, vaccinations, and the ongoing Government use of monetary and fiscal policy to stimulate the economy. Economic growth and company earnings growth have shown supranormal recoveries from the depths of lockdown.

The big question as we enter the second half of the year is, can this continue given the spread of the delta variant? The authorities seem comfortable with the pick-up in inflation and are determined to maintain support for worldwide economies.

This month, once again we look at various aspects of current market conditions and what that might mean going forward.

More upside to come?

The US earnings season is with us again, which is when a large number of publicly traded companies release their quarterly earnings figures, and there is the expectation that earnings growth will be 64% for the second quarter which, if materialised, would be the second-best year-on-year quarterly gain in the last 25 years.

This expectation has led to markets pricing in this “supernormal” growth which raises the risk that if the figures don’t quite live up to expectations, any undershoot would challenge those current valuations in equity markets. However, as we all emerge from a global Pandemic and with lockdown restrictions beginning to be lifted, the environment is ripe for Companies to achieve higher earnings.

Investors will also be keeping an eye on Company commentary about rising prices and, if we do see this, what will the forecast impact of this be on future earnings. At present, expectations of earnings for the third quarter of the year are strong, but we may see a shift in this, if there are any earnings revisions made over the next few weeks.

Yields paused

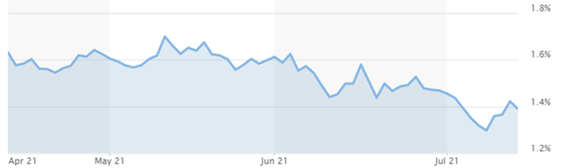

The yield refers to how much income an investment generates and as we have indicated before, as prices rise, yields tend to fall and vice versa.

In February we saw inflationary concerns come to the fore as the improvement in Vaccination distribution increased the markets expectations for future growth and further inflation. This led to investors selling out of bonds, which in turn increased the yield.

Table 1: US 10yr yield (Source: MarketWatch)

However, we have since seen yields fall again with the US 10 yr. yield falling to a three-month low. There is not an obvious single cause for this, but instead a combination of several factors including:

1. Slowing Global Growth

Recent data from China showed that the bellwether of the COVID-19 recovery is beginning to slow, with the GDP expected growth rate forecast to fall to 8% in the second quarter of the year compared to 18% in the first three months.

A fall is unsurprising, given the base effect of starting from an abnormally high number, but the timing of the fall was a surprise to the market. This also coincided with the People’s Bank of China reducing its reserve requirement, which was introduced to increase the availability of liquid assets to small businesses which have been struggling to return to pre-pandemic activity levels, and perhaps provides an insight into the challenges other Countries will face.

This slowdown in growth (particularly in China) should prove to be disinflationary over the short term as the demand for commodities and capital goods reduces. These two factors (slowing growth and lower inflationary pressures) are tailwinds to bond prices.

2. Central Bank policy and rhetoric

Central Banks now are stuck between a rock and a hard place.

On one side a signalling of a reduction in economic stimulus is greeted by fears that the market will no longer be underpinned by huge amounts of liquidity. Conversely continued stimulus in its current form presents the issue of how economies will wean themselves of this debt induced growth.

We have recently seen members of the Federal Reserve contemplating the reduction of its Asset Purchase Program, which the market viewed as a potential reduction in liquidity, and when this occurs you tend to see investors move from “risk” assets such as equities into “risk off” assets like government bonds. This extra demand can see the price of bonds rise which in turn means yields will fall.

3. Attractive valuations

Bond investors have had a challenging time recently dealing with low yields and the prospects of higher inflation. Yields increasing gave the opportunity for investors to enter the market at a more attractive valuation. This was highlighted in the recent US Government bond auction which saw strong demand.

We have also seen large institutional investors, like pension funds, reduce their allocation to equities (capuring some of the gains they have made) and move into bonds. Bonds have a notable benefit for pension funds as their fixed coupon payment can be used to help fund retiree benefit obligations.

Summary

The overall environment still looks supportive for “risk” assets such as equities, but we are mindful that their could be challenges as the year progresses and we pass the peak pace of recovery. There are still risks that can cause market volatility, so we think that a diversified approach to portfolio construction is sensible.

Please note: This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested: past performance is not a guide to future returns.

![]()