AI drives fundamental not artificial growth in markets

Global equity markets maintained their strong momentum in May, recovering from March lows. This rebound was underpinned by a combination of artificial intelligence (AI) optimism, robust corporate earnings and an easing of geopolitical tensions.

Equity returns, however, remained highly concentrated. For the second consecutive month, technology companies outperformed the broader market, fuelled by the scaling of generative AI and surging hardware demand. Conversely, defensive sectors such as utilities and consumer staples trailed as risk sentiment improved. The energy sector also faced headwinds; oil prices fell below $100 a barrel, recording the sharpest one-month decline since 2020 on expectations that the Strait of Hormuz would soon reopen.

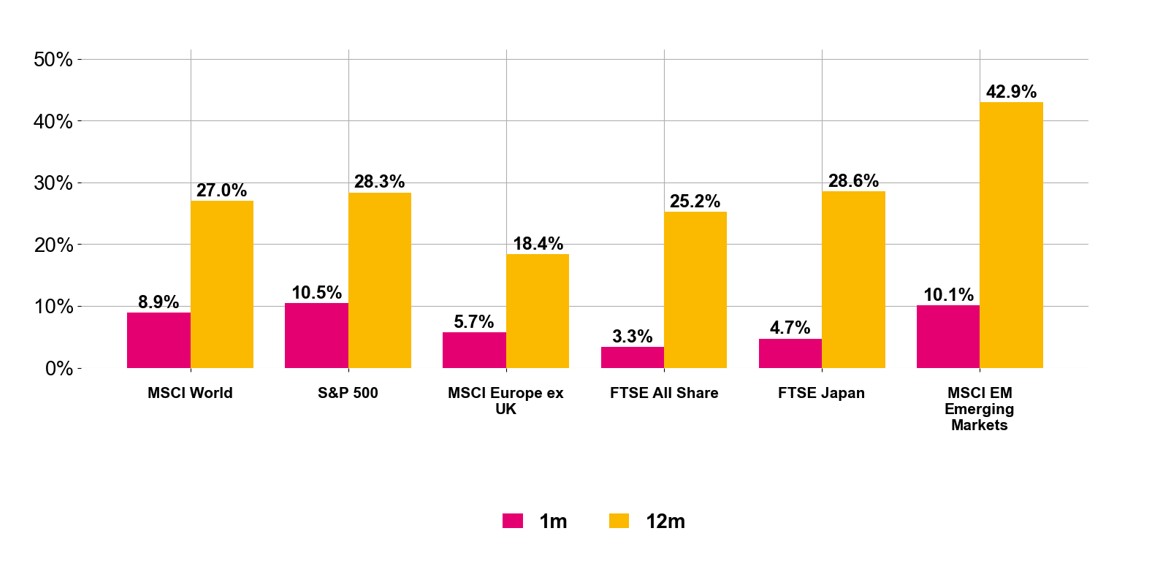

Figure 1. Regional Equity Returns (May 2026, Source: Pacific Asset Management)

This rally particularly benefited regional markets with heavy AI exposure. The US market, home to some of the world’s leading AI innovators, reached new record highs, returning 10.5% in sterling terms and marking its longest weekly winning streak since late 2023.

These gains were supported by another stellar earnings season, with aggregate earnings growing 28.6% year-over-year (YoY). The technology sector led the way with a 54.3% YoY growth rate, driven by notable contributions from Nvidia and Micron, the latter of which officially joined the $1 trillion market cap club in May. Even at the index level, the blended Q1 2026 earnings growth rate of 28.6% sits significantly above the five-year average of 16.4% and the ten-year average of 10.3%.

AI is becoming a driver of economic growth

We are also observing AI capital expenditure which analysts forecast to exceed $1 trillion within two years transcend the micro (company) level to influence macro-economic data. While the U.S. economy grew at a healthy annualised rate of 2% in the first quarter of 2026, a look beneath the surface reveals a fascinating shift in composition: non-residential fixed investment, a proxy for AI infrastructure spend, accounted for nearly 75% of that growth.

The AI-driven capex boom was not confined to the US, Emerging Markets also benefited as investors sought exposure to the AI theme at more attractive valuations than those found among US tech leaders.

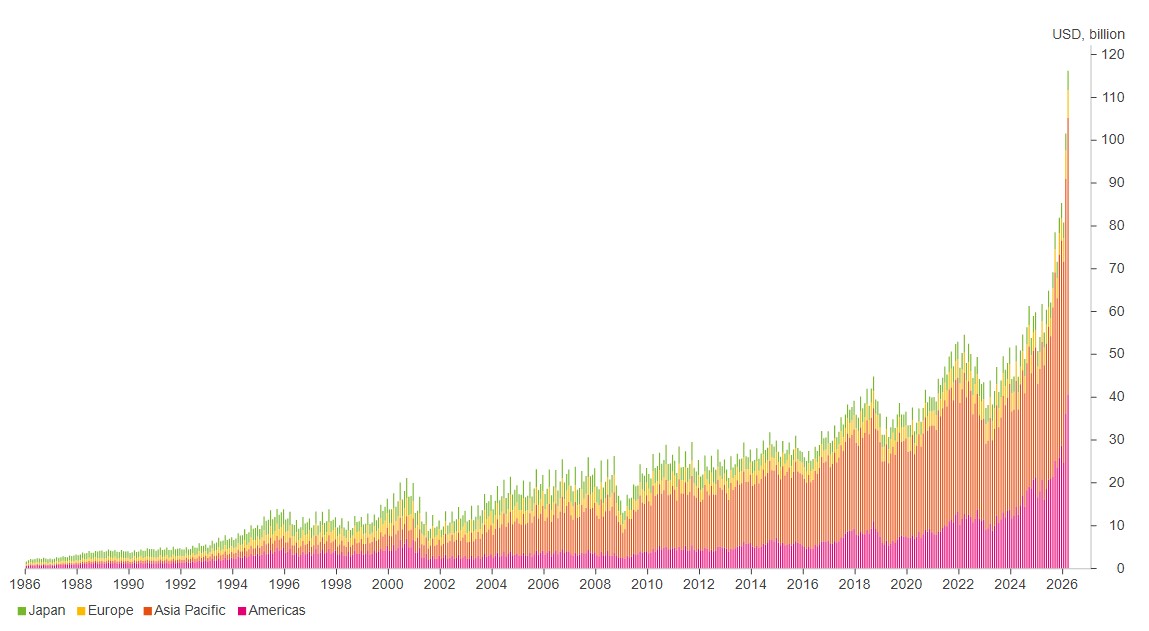

South Korea and Taiwan led regional returns, driven by continued demand for memory chips. This saw SK Hynix and Samsung join the $1 trillion market cap club, reigniting the ‘bubble’ debate. However, while recent price action has been extreme, it is supported by fundamentals: Q1 2026 earnings growth in Asia was exceptional at approximately 40%, one of the strongest quarters in recent history as global demand for semiconductors continues to accelerate.

Figure 2. Demand for Semiconductors (May 2026, Source: PAM, World Semiconductor Trade Statistics)

Fixed income: a diverging picture

May was characterised by a distinct divergence in asset class performance. While equity benchmarks hovered near record territory, bolstered by a historic earnings cycle and the persistent expansion of AI infrastructure, sovereign debt markets remained under pressure. This weakness was driven by concerns over persistent inflation and ongoing uncertainty regarding the trajectory of future monetary policy.

UK Government Bonds emerged as a relative bright spot, outperforming the broader global sovereign market. A cooling labour market and lower than anticipated inflation figures provided the necessary tailwinds to drive yields lower toward month-end. This resilience occurred despite considerable domestic political shifts; local election results showed a sharp decline in Labour support, with the party losing roughly 1,500 seats. This suggests a fundamental realignment of the UK’s political landscape, as the traditional two-party dominance gives way to a fragmented multi-party system featuring a significant rise in support for the Reform Party.

The resulting pressure on Prime Minister Keir Starmer has fuelled speculation regarding potential leadership transitions, with figures such as Andy Burnham and Wes Streeting being discussed as possible alternatives. This heightened political uncertainty has introduced a risk premium, which threatens further upward pressure on UK Government Bond yields.

On the global stage, the environment was more challenging. The US 30-year Treasury yield reached its highest level in nearly two decades after April’s CPI reading showed inflation rising to 3.8%, driven by elevated energy prices. In Japan, sovereign yields climbed to forty-year highs following Prime Minister Takaichi’s announcement of a supplementary fiscal budget designed to shield the domestic economy from rising energy costs.

Conclusion: strong markets, narrow leadership

Global markets remain in a state of fragile equilibrium. While an exceptional earnings season has provided a robust foundation for current valuations, this support is increasingly concentrated within a narrow segment of the technology sector. This resilience in equities stands in stark contrast to the cautionary signals from fixed income and the volatility of the energy market.

Looking toward June, the sustainability of the rally depends on three critical factors: the stability of Brent crude below the $100 threshold, the continued fundamental delivery of the AI investment thesis and the ability of equity markets to navigate an increasingly restrictive yield environment.

Investment Champion uses the expertise of the Investment Team at The Private Office to create simple to understand investment portfolios that offer an alternative and cost-effective way to make your money grow. The Investment Champion portfolios provide diversified investment exposure across a range of geographies and asset classes in order to produce attractive risk-adjusted returns for investors. These portfolios use passive funds which track the performance of a benchmark and are not actively managed by a fund manager. They therefore offer a cost-effective solution to building a portfolio.

The information in this article is correct as at 10/06/2026.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

![]()